VAT On Business Energy Bills Explained

Costs relating to energy have skyrocketed for businesses across the UK. Even with the government attempts to keep costs manageable, the average business is now paying almost double for their energy when compared to before the energy crisis (Pre 2021). Now onto the question at hand, VAT, this is a tax that is paid on energy use. It increases the prices that businesses pay for their energy and can become an added burden you need to account for. But what exactly is VAT, how much will it cost your business and who needs to pay it? Check out our guide below that will tell you all you need to know about VAT on business energy bills.

What is VAT?

VAT stands for Value Added Tax, it is a form of sales tax that is added to the majority of products and services sold by VAT registered businesses. VAT has 3 defined bandings:

- 20% – this applies to most goods and services

- 5% – Applies to some good and services such as domestic energy and children’s car seats

- 0% -for zero rated goods such as foods and children’s clothes.

You can see the governments full list of good and services that VAT applies to here.

Businesses are able to reclaim most of the VAT they are charged by suppliers, and they will also usually collect VAT from the customers they sell to. The charging of VAT begins at the production stage (Such as a manufacturers plant), and continues through the sales pipeline with business paying, claiming back and then re-charging VAT until the pipeline reaches a customer who cannot claim back the VAT – this is usually a not VAT registered business or a private consumer (Member of the public).

By law VAT registered businesses are required to:

- Include VAT in the sale price of the goods or services they provide at the correct rate.

- Keep a record of all VAT paid to suppliers.

- Account for VAT on any goods they have imported to the UK.

- Report the amount of VAT they have charged to customers and how much VAT they have been charged by other businesses. They will then need to send a VAT return to HM Revenue and Customs (HMRC) – usually done every 3 months.

- Pay any VAT they owe directly to HMRC.

Any VAT paid to HMRC is the difference between the amount of VAT the business has been charged and the amount of VAT they have charged tp their customers. If a business has paid more Vat than it has charged to customers HMRC will refund the difference.

Do I need to be VAT registered?

UK law states that you must be VAT registered if:

- You expect your VAT taxable turnover to be more than £85,000 in the next 30-day period.

- Your business had a VAT taxable turnover of more than £85,000 over the last 12 months.

Taxable turnover is your sales of goods and services that would be liable to VAT, (non-exempt).

When you first register for VAT, you will be provided a VAT number, which is your unique VAT identify, which must be included on all invoices and VAT receipts that are given to customers. HMRC will inform you when you are required to submit your first VAT return and payment (If applicable)

Does VAT apply to business gas and electricity?

Yes, businesses in the UK are required to pay VAT on their energy tariffs – both Gas and electricity are charged at 20% unless you’re eligible for a discounted rate of 5%.

How much is VAT on business gas and electricity?

VAT for business gas and electricity is charged at the standard rate of 20%, however some businesses may qualify for the discounted rate of 5% (Please see below)

What is the VAT rate on energy for microbusinesses?

A microbusiness is defined as a non-domestic consumer that meets one of the following criteria:

- Employs fewer than 10 employees (or full-time equivalent) and has an annual turnover or balance sheet no greater than €2 million.

- Uses no more than 100,000 kWh of electricity per year.

- Uses no more than 293,000 kWh of gas per year.

Micro businesses will pay 20% VAT on their energy usages unless they meet one of the following requirements which would make them eligible for the discounted rate of 5%:

Either

- At least 60% of the business’ energy is used for dwelling or residential accommodation.

- They are a charity or non-profit business.

Or they are classed as a low energy user:

- Use less than 33kWh of electricity per day or 1,000kWh per month.

- Use less than 145kwh of gas per day or 4397kWh per month.

If you believe you qualify for a reduced rate, you need to check with your current energy supplier to ensure you are being charged the discounted rate. It has been found that some businesses have been paying the standard rate when eligible for discounted rates, if this is case for your business you may be able to claim a partial refund on any overpayments over the last 4 years. To make a claim, you will need to contact your energy supplier and complete a declaration form.

How do I find how much VAT I’m paying?

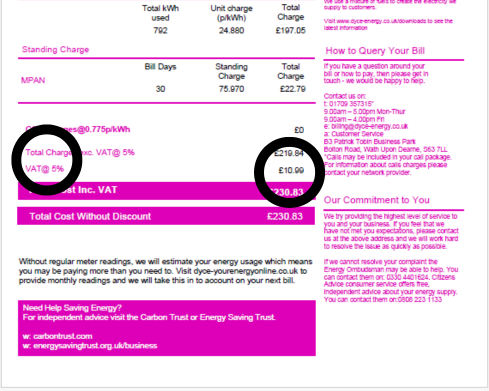

The VAT rate and the amount you have been charged for your energy usage will be displayed on your bill. If you are a Dyce Energy customer this is on the second page of your bill, please see the image below, if your with another supplier, please contact them directly:

Can I claim back VAT on business gas and electricity?

No, VAT is payable on all business energy, regardless of whether you operate from a business premises or work from home. Although purchasing commercial energy is a business-to-business transaction, you are unable to reclaim the VAT in the same way as you would for other business expenses.

Can a charity reclaim VAT?

If the charity is VAT registered and is paying VAT on some goods and services, they may be eligible to claim back the VAT. If the charity is not VAT registered, they are unable to claim back any of the tax.

How about schools and universities?

Yes and no. VAT registered schools and universities that provide education to students are exempt from VAT, this applies state schools, free-paying private schools and state/private colleges and universities.

However, as some VAT registered schools and universities may provide some goods and services to students and the public that are subject to VAT, these are classed as ‘partially exempt organisations’ and can only claim a part of the VAT charged by suppliers.

Some examples of the goods and services that schools and universities provide that would be VAT eligible are:

- Letting of facilities to other organisations.

- Sales of laptops and other technology (even if it is sold at cost or below)

- Commission from photographers.

- Admission charges for events e.g plays, concerts etc.

- Goods sold on the campus e.g student unions, campus shops etc.

- Vending machine sales.

Is VAT charged on the climate change levy (CCL)?

The Climate Change Levy (CCL) is a tax that is designed to encourage UK businesses to be more sustainable. In simple terms the CCL deters business energy users from consuming energy that creates carbo emissions – the more energy efficient your business is, and the less it uses carbon creating energy, the less CCL you will pay.

VAT is also charged on the CCL – yes, it is a tax on a tax – so the figure you see for your CCL on your bills is typically 20% higher as VAT is charged.

How can I make even further savings?

With energy costs continuing to soar, organisations are aiming to reduce their costs to stay competitive.

To make savings on your energy, it all begins with your energy bills. Ensure you are paying the lowest rate of VAT you are eligible for, are on the best energy tariff available to your business and you are claiming every refund and exemption you are entitled for.

If you are looking to switch energy providers, you can get our most competitive rates by completing our 2 minute switching form here.